ACORD 855 in New York Construction: What It Confirms That a COI Doesn’t

Most people in New York construction know what a COI is.

You request it. You receive it (sometimes). You file it. You move on. And if the universe is feeling generous, nothing catastrophic happens between “certificate received” and “project completed.”

The part New York adds—quietly, consistently, and usually at the least convenient time—is the ACORD 855.

Not because New York loves paperwork (although it does).

Because the standard COI is too vague about the very details that decide whether coverage behaves the way everyone assumes it will.

And that’s the whole point of the 855: it takes a bunch of fuzzy assumptions and asks them to become specific answers.

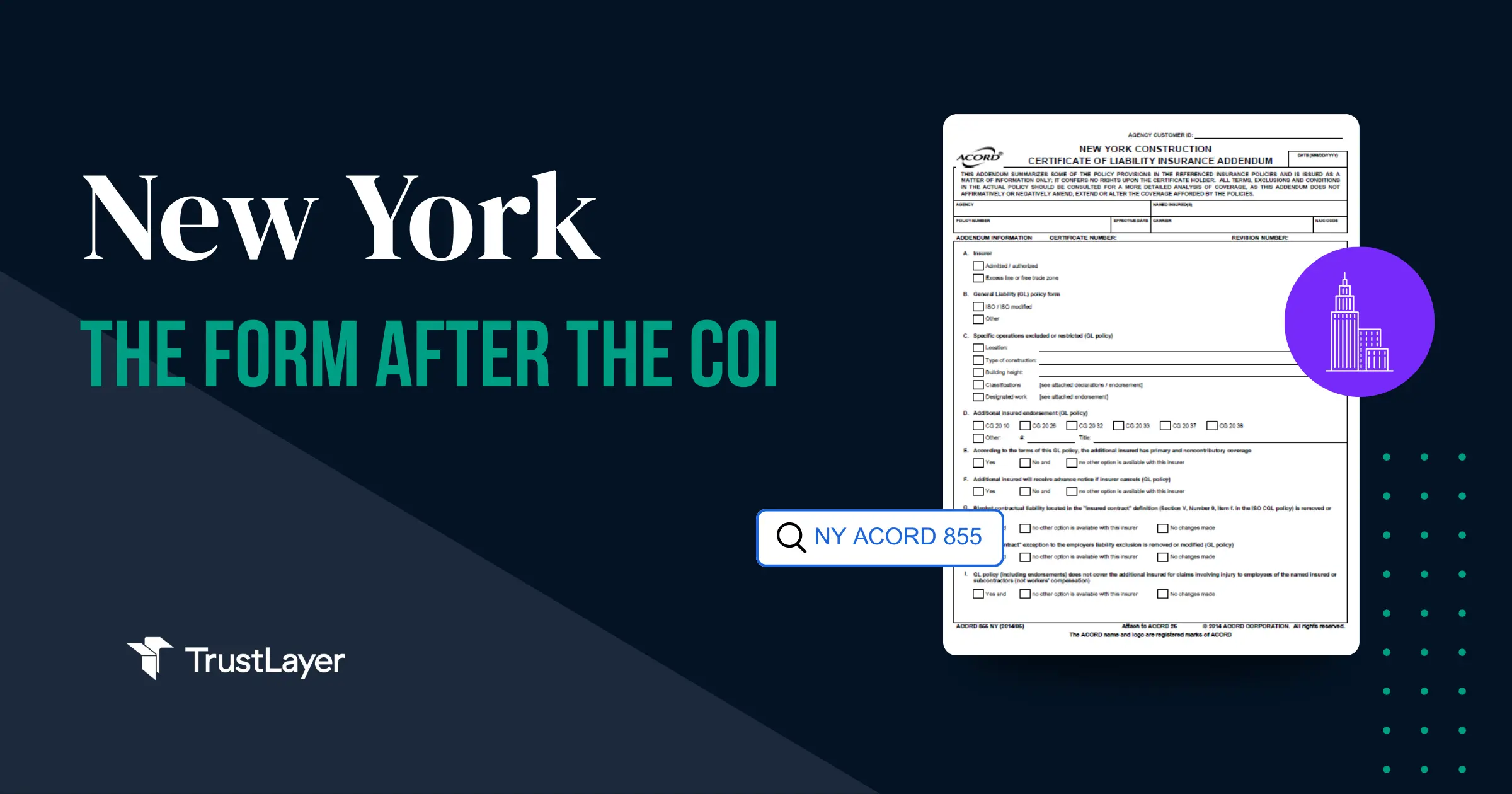

What Is the ACORD 855?

The ACORD 855 is an addendum often requested in New York construction that affirms whether certain coverage terms are present on a subcontractor’s General Liability (GL) policy.

It’s not a replacement for the COI. It’s not a policy. It’s not a magic shield.

It’s a structured way to confirm details that a COI often implies without actually proving them.

Why New York Uses the 855

A COI typically communicates:

- policy type (GL, auto, umbrella, etc.)

- limits

- dates

- certificate holder info

- some endorsement references (sometimes)

What it does not reliably communicate is the way coverage functions under stress—meaning when there’s a claim, a tender, a dispute, or an “okay but whose policy pays first?” situation.

The 855 exists because New York construction risk tends to collide with these questions:

- Does the Additional Insured status actually apply the way the contract expects?

- Is it primary and non-contributory, or is that conditional?

- Does completed operations respond the way the job requires?

- Is contractual liability intact or narrowed?

- Does the umbrella/excess follow the same rules or play by its own?

The 855 turns those into checkable answers. That’s the intent.

The Flip Moment: “Collecting Documents” Isn’t the Same as “Managing Risk”

Here’s the uncomfortable truth New York paperwork tends to reveal:

A compliance program can be excellent at collecting documents and still be bad at preventing exposure.

Because exposure isn’t created by missing PDFs.

Exposure is created by unclear coverage expectations and undefined outcomes.

The 855 doesn’t just add a form. It adds a moment of clarity:

“If the answer is No, does anything actually change?”

If the honest answer is “not really,” then the form is decorative.

If the answer is “yes, we have a defined response,” then the form becomes useful.

What the ACORD 855 Typically Confirms

Different programs care about different items. But these are the usual heavy hitters—the fields that tend to matter because they affect real loss outcomes.

1) Additional Insured: Primary and Non-Contributory (PNC)

What it’s getting at: If there’s a claim, will the subcontractor’s coverage respond first without pulling the GC/owner into the payment stack?

PNC isn’t a vibe. It’s a coverage posture.

And in a claim scenario, posture becomes expensive quickly.

2) Blanket Contractual Liability

What it’s getting at: Does the policy support the insured’s contractual obligations (including certain indemnity obligations), or are there carve-outs and restrictions?

This matters because contracts are written on the assumption that the GL policy can “backstop” certain promises. Sometimes it can. Sometimes it can’t.

3) Completed Operations

What it’s getting at: Does coverage respond after the work is done (not just while it’s happening)?

Completed operations claims are not theoretical.

They are basically the entire genre of “everything was fine until it wasn’t.”

4) Umbrella/Excess Behavior (Including PNC for AIs)

What it’s getting at: Does the excess/umbrella follow form and extend the same protections—or does it behave differently?

Extra limits don’t automatically equal extra protection if the mechanics don’t match.

What to Do With the 855 Without Becoming an Insurance Lawyer

This is the part where most teams either:

- pretend it’s all the same, or

- disappear into the weeds and never come back.

There’s a middle path.

Step 1: Identify Which Items Are “Program-Defining”

Not every item deserves the same emotional response.

Most programs end up with three categories:

- Deal-breakers (must be “Yes”)

- Decision items (depends on scope, trade, or job type)

- Nice-to-haves (worth tracking, not worth derailing a project)

Step 2: Decide What a “No” Means

This is the part people skip because it requires committing to a real operational stance.

A “No” can mean:

- follow-up request for clarification

- request for endorsement/policy change

- conditional approval

- exception/waiver with documentation

- disqualification (rare, but sometimes real)

The form isn’t the value. The defined response is.

Step 3: Keep the Outcome Consistent

Consistency is not about being harsh. It’s about being credible.

If the exact same “No” produces:

- a hard stop on one job,

- a shrug on another,

- and an exception nobody documents on the third…

…then the program isn’t risk-managed. It’s mood-managed.

Common Misunderstandings About the ACORD 855

“If we have the COI, we’re fine.”

The COI is necessary. It’s rarely sufficient in New York construction. The 855 exists because the COI does not reliably confirm the mechanics that matter.

“The 855 proves the policy.”

It doesn’t. It’s a form. But it’s a form designed to force clarity where the COI stays vague.

“If the sub checks ‘Yes,’ we’re good.”

A checked box is not the end of the story. It’s the start of a clearer story—one that should align with your program’s expectations.

Frequently Asked Questions Acord 855

Q: Is the ACORD 855 required in New York construction?

It commonly comes up in New York construction programs and is frequently requested by GCs/owners. Exact requirements vary by project and contract.

Q: What does the ACORD 855 add beyond the COI?

It confirms specific GL policy terms—especially regarding Additional Insured status, primary/noncontributory posture, completed operations, contractual liability, and umbrella coverage.

Q: If a subcontractor can’t meet an item on the 855, does that automatically mean disqualification?

Not automatically. It depends on your program rules. The key is to define which items are deal-breakers and what the response should be when the answer is “No.”

Q: Does the 855 replace endorsements or policy review?

No. It’s a structured form that helps surface key coverage terms. It doesn’t replace reviewing endorsements when deeper verification is needed.

Get Clarity on the 855

The ACORD 855 is one of those forms that doesn’t look dangerous until you realize it’s answering questions your COI never actually promised to answer.

If you want a quick second set of eyes on how your current process handles it (and where it quietly falls apart), book a short conversation with TrustLayer.

You might also like