Insurance Tracking for Lenders: Why Manual Borrower Coverage Tracking Breaks Down

Commercial lending is supposed to feel structured.

That is part of the promise. There are files, approvals, diligence checklists, required documents, conditions, and carefully staged decisions built on the idea that expensive things should not move forward until key information is known.

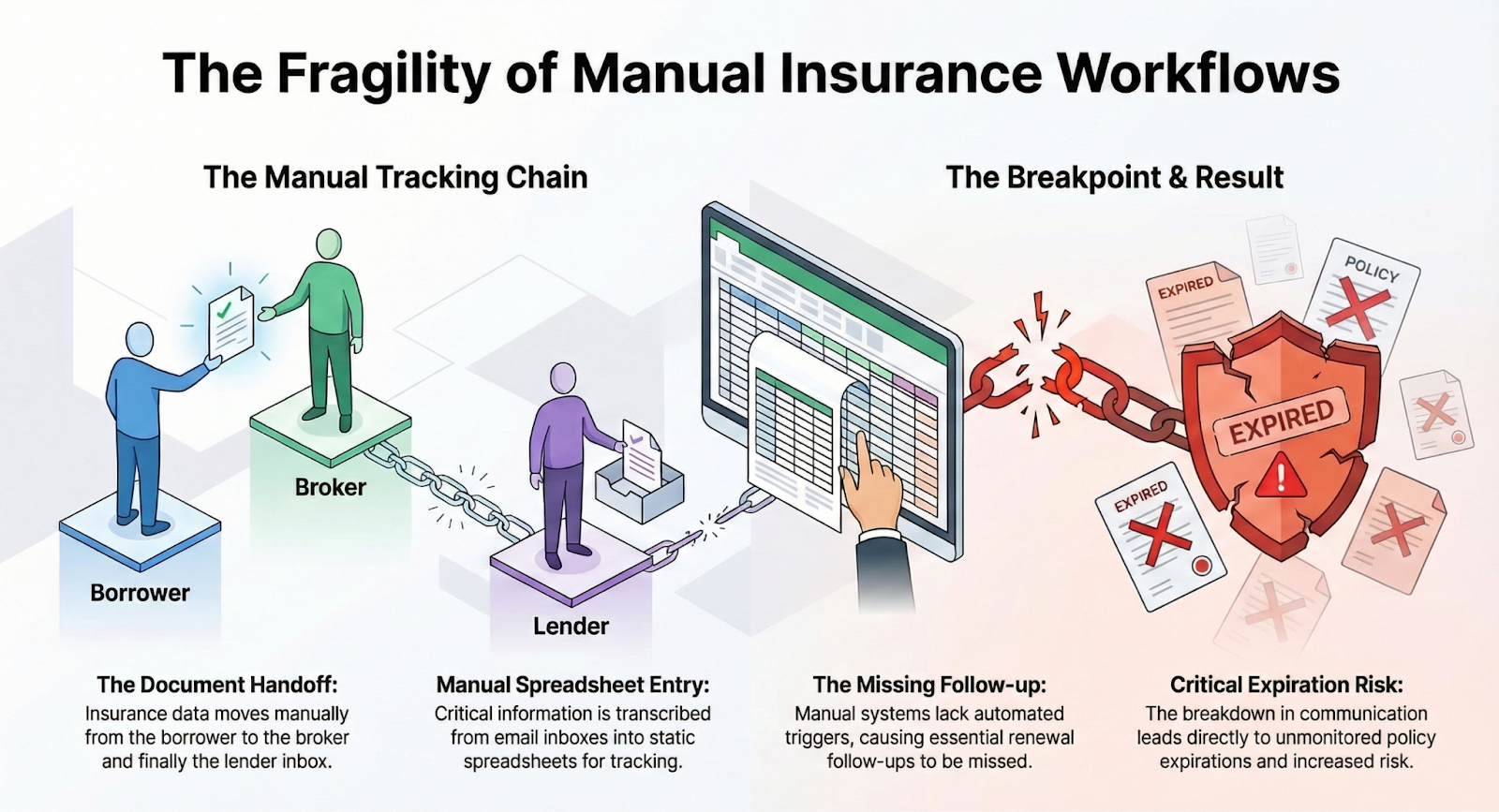

Which is why it is always a little strange to see how often insurance tracking for lenders still lives in a process that feels held together by email threads, spreadsheet tabs, forwarded attachments, shared folders, calendar reminders, and the institutional memory of one very capable person who knows where everything is—until they are out for the day and everyone else realizes the system had more human scaffolding than anyone admitted.

That kind of setup can limp along for a while.

Then the file gets complicated. Or the portfolio gets larger. Or the loan moves from origination to servicing. Or a renewal date sneaks up on you sooner than expected. Or a borrower with three LLCs submits the correct document under the wrong entity name.

And suddenly, the process that seemed merely annoying becomes something worse: fragile.

That is the actual issue.

Insurance tracking for lenders is the process of collecting, reviewing, monitoring, and maintaining borrower insurance documentation across origination, closing, servicing, and renewals. When that process is manual, it tends to break down not because the work is unimportant, but because the work spans too many people, too many files, too many timelines, and too many opportunities for status to become unclear.

This is not just a certificate problem.

It is a visibility problem.

And in lending, visibility problems do not stay small. They become workflow, timing, servicing, reporting, and risk problems. Not because nobody cares, but because manual borrower coverage tracking becomes brittle the moment the loan file becomes more complex than a single document attached to a single moment in time.

Who This Article Is For

This article is for:

- Commercial real estate lenders

- Construction loan teams

- Loan servicing teams

- Portfolio risk and compliance teams

- Lending operations leaders managing borrower insurance requirements

If your team is collecting, reviewing, monitoring, or following up on borrower insurance documentation, this is your problem too.

Key Takeaways About Insurance Tracking for Lenders

- Manual borrower insurance tracking creates visibility gaps across origination, servicing, and renewals.

- Insurance tracking for lenders is more than just certificate collection.

- Commercial real estate and construction lending make borrower coverage tracking more complex because of multiple entities, properties, and changing requirements.

- Loan servicing insurance tracking matters after closing because coverage can lapse, renew, or change over time.

- A better process gives lenders clearer visibility into missing, expiring, and compliant documentation without relying on spreadsheet heroics.

Why Insurance Tracking Matters for Lenders

Lenders collect insurance information because it serves a real operational purpose.

It helps confirm that required coverage is in place, that documentation aligns with the loan file, and that the lender has a clearer picture of whether the borrower relationship reflects the protections it is supposed to reflect. In commercial real estate lending, construction lending, and servicing environments, especially, this matters because documentation is tied directly to real assets, real exposure, and real consequences when something is incomplete, outdated, or missing.

The issue is that insurance tracking rarely stays simple for long.

What begins as “collect proof of coverage” can expand into a layered process involving multiple borrowers, legal entities, properties, project phases, endorsements, renewals, and handoffs between teams. Which means the real work stops being about whether a document exists and starts being about whether anyone can clearly see what is true across the life of the loan.

And that is the shift.

Because insurance tracking for lenders is not just a pre-closing task, it touches origination timelines, construction or build-out phases, servicing workflows, and post-closing monitoring. A manual process may survive one part of that lifecycle. It tends to break when asked to survive it all.

If this feels familiar, you might also find it useful to read TrustLayer’s lending-focused breakdown on where closing workflows tend to stall: Lending Operations Risk Guide: Collateral, COIs, and Three Traps That Stall Closings.

How Insurance Tracking for Lenders Works

At a basic level, lender insurance tracking should help teams do five things well:

- Request borrower insurance documentation

- Review it against lender requirements

- Identify what is missing or incorrect

- Monitor renewals and changes over time

- Maintain visibility across loan stages and internal handoffs

That sounds manageable when written as five clean bullets.

In practice, though, the work often passes through borrowers, brokers, agents, loan officers, operations teams, servicing teams, and compliance reviewers. Documents arrive in different ways. Requirements vary. Timelines move. Renewals overlap. Files get touched by multiple people. What begins as a straightforward document request becomes an ongoing visibility challenge.

That is why manual processes struggle. The work is not isolated. It is connected.

For a simple baseline on what COI tracking is (and why it becomes an operational system, not a one-time task), see The Basics Of Certificate Of Insurance Tracking.

Why Manual Borrower Insurance Tracking Breaks Down

Manual insurance tracking has a talent for looking reasonable right up until the scale shows up.

A spreadsheet seems fine. Shared folders are organized. Email follow-up seems manageable. A checklist gives everyone the reassuring sense that a process exists. In a low-volume environment, that may be enough for a while.

Then the file gets more complicated.

A borrower has multiple LLCs. A project adds construction-stage requirements. A broker sends one document but not another. A revised certificate comes in with a new effective date. Renewals start overlapping. A servicing team inherits a portfolio without full context. Different people touch the same file at different stages and with different assumptions about what has already been handled.

At that point, the manual process stops being a system and starts being a collection of effort.

And effort is not the same thing as visibility.

That is the trap. Teams can be extremely busy—requesting, reviewing, renaming, uploading, reconciling versions, updating trackers—and still not have a fast, confident answer to the most important questions:

What is missing?

What is expiring?

What changed?

What is compliant today?

What needs attention first?

When the answers are slow, the process tells itself.

Where Manual Insurance Tracking Usually Breaks

The weak points are familiar enough that teams sometimes mistake them for normal operational friction. They are not. They are symptoms of a brittle process.

Intake happens across too many channels.

Documents come from borrowers, brokers, agents, and internal teams in different formats and through different channels. Some arrive complete. Some do not. Some get attached to the right file. Some sit in inboxes waiting for “later.”

Review depends too much on memorization.

Manual borrower insurance tracking often relies on checklists, personal experience, or repeated interpretation. That makes consistency difficult, especially as portfolios grow or responsibilities move between origination and servicing.

If your team is constantly decoding and re-decoding COIs, it’s worth linking to a practical explainer, such as Certificates of Insurance: A TrustLayer Guide (2025).

Follow-up becomes repetitive

A missing document leads to an email. Then another email. Then a clarification. Then a correction request. Then another wait. At some point, the process begins to look less like operations and more like professionally managed chasing.

Renewals create quiet exposure.

A file that was complete once can drift out of date without much noise. If no one has clear visibility into upcoming expirations or coverage changes, the gap can remain hidden until something forces it into view.

For a broader view on improving renewal visibility and compliance continuity in lending workflows, see How Automation Enhances Insurance Compliance for Real Estate Loan Providers.

Reporting becomes harder than it should be

When leadership, auditors, or regulators ask for status, manual systems rarely produce clean answers immediately. They produce search exercises, reconciliations, and a lot of “give us a minute.”

This ties closely to what COI compliance actually means in practice and why it becomes a repeatable verification process, not an ad hoc check.

Ownership gets blurry

Origination assumes servicing has it. Servicing assumes the file came over complete. The borrower thinks the broker handled it. The broker believes the revised version has already been sent.

Responsibility exists everywhere and nowhere at once.

That is how gaps survive. Not through one dramatic failure, but through a sequence of small weak points no one can see all at once.

Commercial Real Estate Loan Insurance Requirements Create More Complexity

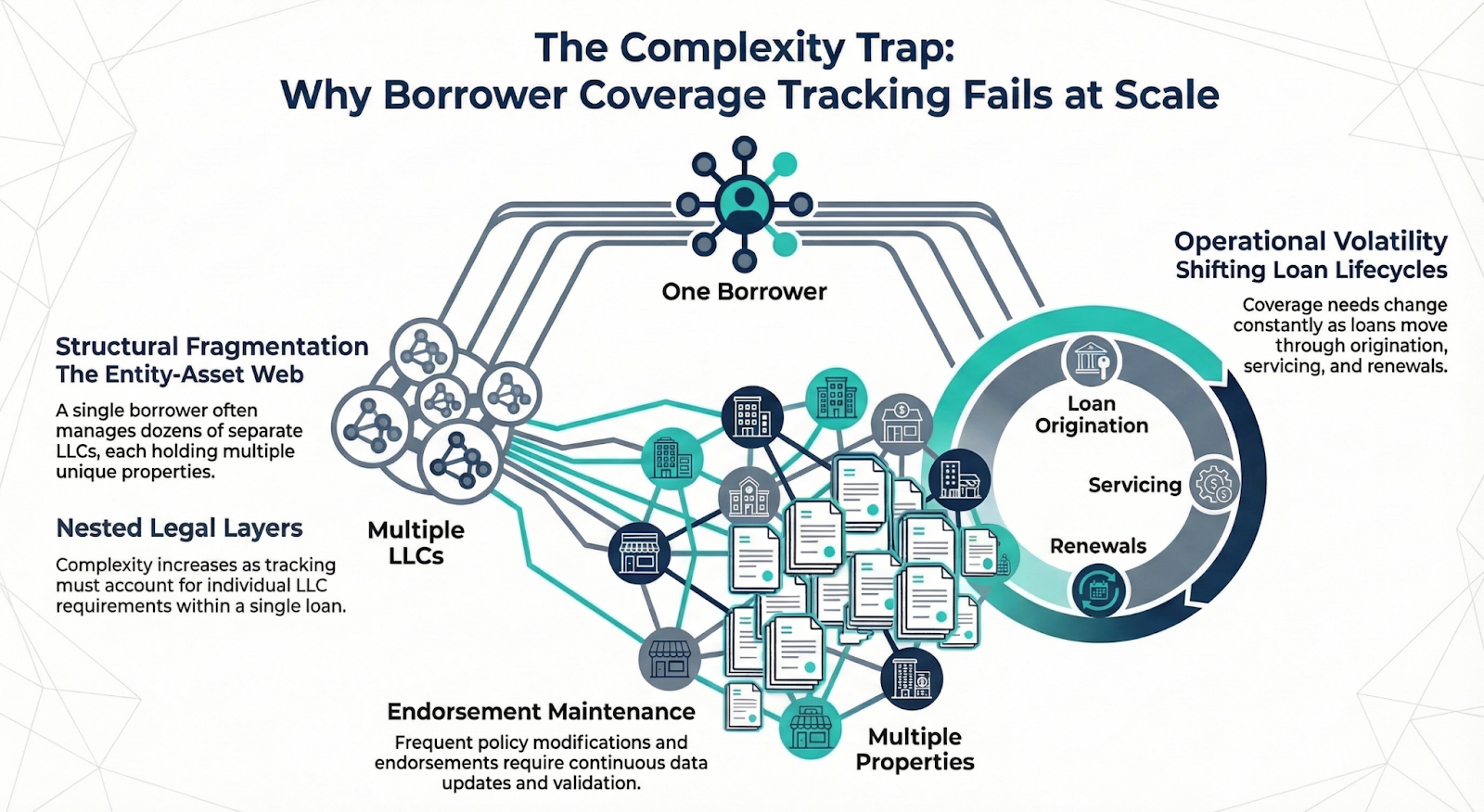

Commercial real estate lending has a way of taking a simple-sounding task and revealing, almost immediately, that it is anything but.

One borrower may control multiple entities. One relationship may span multiple properties. A deal may involve retail, office, industrial, or multifamily assets with different exposures and requirements. Add construction or renovation activity, and now there are more parties, more phases, more documents, and more ways for status to splinter across the process.

This is where the question changes.

It is no longer just: did we receive the certificate?

Now it becomes:

- Which entity is this tied to?

- Does it align with the property and loan structure?

- Are the lender’s insurance requirements actually met?

- Is supporting documentation still missing?

- Has the policy changed since its origination?

- What expires next?

- Can servicing see the same status as the original?

- If someone asked for proof today, could we produce it cleanly?

That is why commercial real estate loan insurance requirements make manual tracking harder. The challenge is no longer collection. The challenge is maintaining a coherent view of borrower coverage across entities, properties, phases, and time.

Why Certificates of Insurance Are Not Enough for Lenders

Certificates matter. They are visible, tangible, and easy to treat like the finish line.

But one of the easiest mistakes in lender insurance tracking is assuming that receiving a certificate means the insurance question has been handled. Often, it means only that one visible piece of the file has arrived.

What lenders actually need is clarity.

They need to know whether the right entity is covered, whether the documentation aligns with the requirement, whether supporting pieces are present, whether the dates still hold, whether the file remains current after closing, and whether the same status can be understood across teams without requiring a dramatic amount of manual reconstruction.

That is why this is not just a certificate problem.

It is a visibility problem across a changing loan lifecycle.

And once you see it that way, a lot of things start making more sense. Why teams feel busy but not always confident. Why are renewals becoming a scramble? Why servicing teams inherit ambiguity. Why does reporting take longer than it should?

For teams looking to standardize “what good looks like,” here’s a useful reference: Insurance Verification Best Practices for Efficient COI Tracking.

Loan Servicing Insurance Tracking Matters After Closing

One of the more dangerous assumptions in lending is that insurance tracking is mostly a pre-closing concern.

That would certainly be convenient.

In reality, loan servicing insurance tracking matters because the facts keep changing after closing. Policies renew. Coverage shifts. Borrowers change carriers. Documents expire. Requirements still matter. The file may have been complete once, but “complete once” is not the same thing as “visible now.”

This is why servicing teams need more than inherited attachments and vague assurances that everything critical has already been handled upstream.

They need to know:

- What is the current

- What is missing

- What is approaching expiration

- What changed

- What requires follow-up before it becomes a bigger issue

In manual systems, this often turns into reactive work. The team is not monitoring so much as rediscovering. And rediscovery is a poor operating model for anything tied to collateral, compliance, or lender risk.

What Better Insurance Tracking for Lenders Actually Looks Like

A better process is not just “less manual.” That is true, but too vague to be useful.

What lenders really need is a way to reduce ambiguity.

Better insurance tracking for lenders should make it easier to:

- Understand borrower coverage status quickly

- Track requirements by loan, entity, property, or phase

- Identify missing or expiring documentation earlier

- Reduce repetitive follow-up

- Create continuity from origination through servicing

- Support cleaner reporting and audit-readiness

- Maintain visibility without relying on side notes and memory

That is the value. Not just storage. Not just a collection. Not just one more place to keep files.

The real value is being able to answer important questions without turning them into group projects.

Because if the question “What is our borrower insurance status?” still requires inbox searches, spreadsheet reconciliation, and several people comparing notes, the process is not creating confidence. It is creating labor.

For more on why the shift to digital verification changes the operating model (especially around proof, timeliness, and access), see The Impact of Digital Proof of Insurance on Compliance Tracking.

The Real Cost of Staying Manual

The cost of manual borrower coverage tracking is easy to underestimate because much of it is hidden in the background.

It hides in slower loan workflows.

It hides in extra follow-up.

It hides in servicing handoff friction.

It hides in reporting delays.

It hides in uncertainty that forces people to double-check what should already be clear.

It hides in the dependence on a few experienced team members who keep the process functioning through sheer effort.

That kind of cost does not always show up neatly on a line item. But it keeps showing up in operations.

And in lending, operational uncertainty has a way of becoming expensive even when it starts small.

If you want a clean “why this matters” supporting link that ties time savings to operational clarity, use: Five Ways Insurance Tracking Saves Organizations Time.

Lenders Do Not Need More Spreadsheet Heroics

One reason manual systems survive as long as they do is that smart people become very good at compensating for them.

They remember exceptions. They keep extra notes. They build side trackers. They know who to email. They know which version is right. They become the safety net.

Which is admirable—right up until the business starts depending on that as the plan.

Because the goal is not to find stronger people willing to carry a fragile process longer, the goal is to build a process strong enough that it does not keep asking people to rescue it.

For lenders, that means borrower insurance tracking needs to be more visible, more consistent, and less dependent on scattered communication and manual reconstruction. It needs to hold up across origination, construction, or build-out phases, servicing, renewals, and the ordinary complexity of commercial lending relationships.

Because when manual insurance tracking breaks down, it rarely happens all at once. It breaks one missed follow-up, one unclear handoff, one quiet expiration, one disconnected file at a time.

Which is exactly why it deserves more attention than it usually gets.

Insurance Tracking for Lenders: Frequently Asked Questions

Q: What is insurance tracking for lenders?

Insurance tracking for lenders is the process of collecting, reviewing, monitoring, and maintaining borrower insurance documentation across the life of a loan. It helps lenders maintain visibility into required coverage, renewals, and compliance status.

Q: Why does manual borrower insurance tracking break down?

Manual borrower insurance tracking breaks down because documents arrive through multiple channels, requirements vary by loan and property, renewals create ongoing work, and status gets spread across email, spreadsheets, and disconnected files.

Q: Why is insurance tracking important for commercial real estate lenders?

Commercial real estate lenders often manage multiple entities, properties, and insurance requirements within a single relationship. Insurance tracking helps create better visibility across origination, servicing, renewals, and collateral-related risk.

Q: Is a certificate of insurance enough for lenders?

Not always. A certificate may be one part of the file, but lenders often need broader visibility into entities, limits, dates, endorsements, and requirement-specific documentation.

Q: Why does loan servicing insurance tracking matter after closing?

Loan servicing insurance tracking matters because coverage can lapse, renew, or change after closing. Lenders need ongoing visibility into borrower compliance, not just a one-time pre-closing collection process.

Q: What should lenders look for in a better insurance tracking process?

Lenders should look for clearer borrower visibility, easier renewal tracking, less manual follow-up, better continuity between origination and servicing, and cleaner status reporting across loans and properties.

See a Better Way to Manage Insurance Tracking for Lenders

When borrower coverage tracking lives across inboxes, spreadsheets, and scattered follow-up, visibility gets harder right when it matters most.

TrustLayer helps teams reduce manual insurance tracking and create a clearer process across origination, servicing, and ongoing compliance workflows. Schedule time to chat today.

You might also like